Michalis A. Michael

December 9, 2021

We do not have proof of causality yet, but the 92% correlation between sentiment and stock price should be a wake-up call.

What do 25,000+ online posts say about Portuguese banks? A revealing look at customer sentiment shows why some banks should be paying closer attention.

.webp)

They say a picture is worth a thousand words. Perhaps even more judging from the graphs below and the compelling story they tell on bank performance!

In October 2021, listening247 carried out a social intelligence (SI) project about banks in Portugal, it’s 5th project in the industry, to illustrate the value of unsolicited customer opinion to a bank’s management.

The opinions were “unsolicited” in the sense that no one asked anyone a question; the only source used was online sentiment as expressed on Twitter, Facebook, blogs, forums, videos, reviews and the news.

25,758 unique posts were gathered about 13 banks from all these sources from September 1st , 2020 to August 31st, 2021.

Novo Banco has the highest share of voice at 54% followed by MIllenium BCP with 40% and Santander with 18%. On the other end of the positive-negative spectrum, we have four banks each with fewer than 200 posts in an entire year.

The question is: is it a good thing to have the highest share of voice (SoV) in a competitive market?

Not necessarily…it depends!

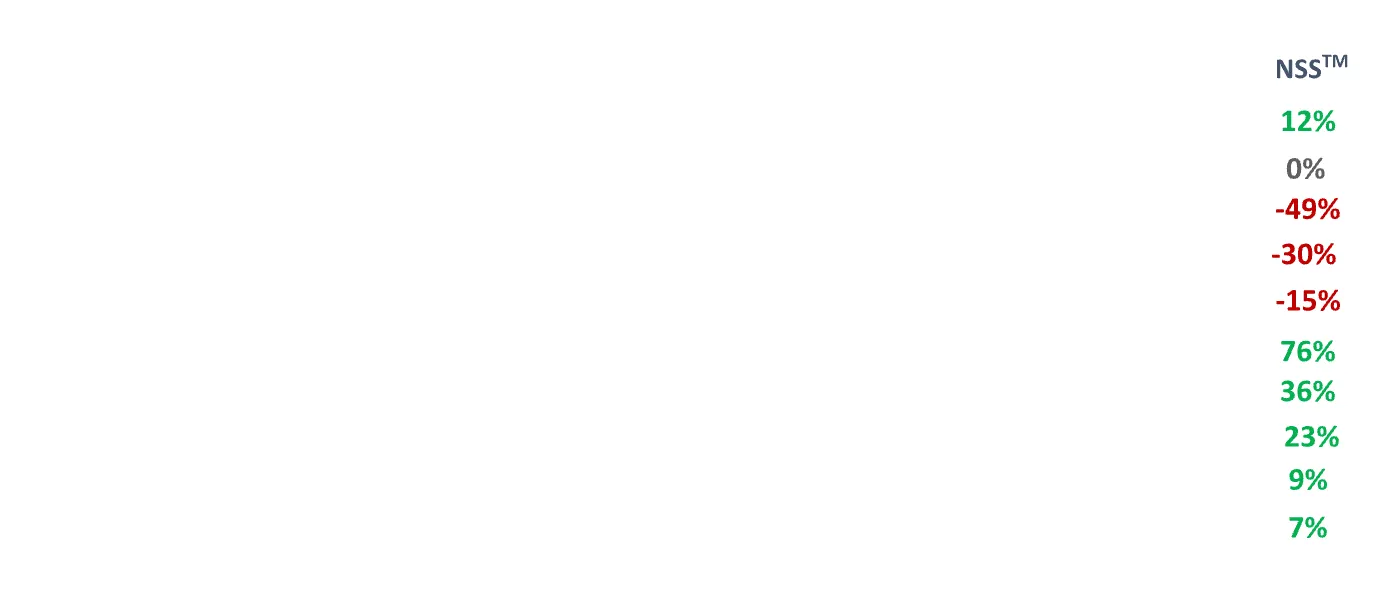

In the case of Novo Banco, the SoV is bad news. Most of the posts about them express negative sentiment – the red bars on our graph express a net sentiment scoreTM (NSSTM).

The NSSTM basically means that there are more negative posts than positive, for 8 out of the 13 banks included in the analysis.

Caixa Central has the worst NSSTM at -46% followed by Novo Banco with -42%.

So, what is the reason for the negative sentiment?

Well, it is mainly about the customer experience – a whopping 16,881 posts - and Novo Banco leads with 51% share of negative sentiment, considerably more than the corresponding score for Millenium BCP (24%). The 3rd highest share of negative CX was for Santander.

Interestingly, Santander is one of the 5 banks with positive NSS overall, perhaps on account of their active Facebook presence and higher customer engagement.

However, if we just look at the news, Santander’s NSS is slightly negative at -4% albeit still way better than the corresponding figure for Novo Banco (-45%).

In Fig.4 below we compare the NSS for Portugal’s main banks with other industries and product categories as well as with selected global banks.

What transpires is that banking in Portugal is among the three worst sectors in terms of negative sentiment along with public transportation in the UK and telecommunications in the Netherlands. Even within banking, Portugal’s lag in performance (compared to other countries or regions) is starkly evident.

Fig 5. below - for 11 Global Banks - is the equivalent of Fig. 2 where we show the NSS ranking for Portuguese banks. The difference could not be starker; the red is replaced by green – which means that 10 out of 11 banks have positive NSS albeit recorded one year earlier than for Portugal.

To be fair, the sentiment towards banks seems to change drastically depending on the economic situation. Negative sentiment appears to get a boost during an economic downturn or a recession. It improves when times get better.

Most traditional bankers are very slow to adopt innovation perhaps because they are trained to be risk averse. Unsurprisingly, when we showed Fig. 2 to a number of Portuguese bankers their reaction was to immediately question the validity of the data. What is more, they asked to see proof that negative NSS has bottom line implications for those banks.

Peter Nathanial the Board Chairman of DMR and former Group Chief Risk Officer of the Royal Bank of Scotland said about the report: “Social intelligence sourced insights seem to polarise board members and top executives of banks everywhere; at one end, people remain unconvinced that social intelligence provides any insights and want to see proof or causality with their business performance, whilst at the other end, people believe that this data is very powerful and definitely needs to be an important part of their future decision-making process. If the first group is right, then the second group is moving too soon. However, if the second group is right, the first group – and their institutions - will be left behind.”

If the latter group is right, then it follows that the 8 banks in Portugal with negative net sentiment score are losing value by not paying attention on what their customer say online.

We do not have proof of a causal link to their bottom-line performance yet, but we do have the next best thing: data that shows extremely high correlation of sentiment expressed in news and social media with the banks’ stock price.

Check out the last figures below (Fig. 6 & 7) from our report with 11 Global Banks in 2019, which also serve as the conclusion of this post.

I am tempted to say I rest my case. What do you think?